Nonlinear Convex Optimization¶

In this chapter we consider nonlinear convex optimization problems of the form

The functions \(f_k\) are convex and twice differentiable and the linear inequalities are generalized inequalities with respect to a proper convex cone, defined as a product of a nonnegative orthant, second-order cones, and positive semidefinite cones.

The basic functions are cp and

cpl, described in the sections

Problems with Nonlinear Objectives and Problems with Linear Objectives. A simpler interface for geometric

programming problems is discussed in the section Geometric Programming.

In the section Exploiting Structure we explain how custom solvers can be

implemented that exploit structure in specific classes of problems.

The last section

describes the algorithm parameters that control the solvers.

Problems with Nonlinear Objectives¶

-

cvxopt.solvers.cp(F[, G, h[, dims[, A, b[, kktsolver]]]])¶ Solves a convex optimization problem

(1)¶\[\begin{split}\begin{array}{ll} \mbox{minimize} & f_0(x) \\ \mbox{subject to} & f_k(x) \leq 0, \quad k=1,\ldots,m \\ & G x \preceq h \\ & A x = b. \end{array}\end{split}\]The argument

Fis a function that evaluates the objective and nonlinear constraint functions. It must handle the following calling sequences.F()returns a tuple (m,x0), where \(m\) is the number of nonlinear constraints and \(x_0\) is a point in the domain of \(f\).x0is a dense real matrix of size (\(n\), 1).F(x), withxa dense real matrix of size (\(n\), 1), returns a tuple (f,Df).fis a dense real matrix of size (\(m+1\), 1), withf[k]equal to \(f_k(x)\). (If \(m\) is zero,fcan also be returned as a number.)Dfis a dense or sparse real matrix of size (\(m\) + 1, \(n\)) withDf[k,:]equal to the transpose of the gradient \(\nabla f_k(x)\). If \(x\) is not in the domain of \(f\),F(x)returnsNoneor a tuple (None,None).F(x,z), withxa dense real matrix of size (\(n\), 1) andza positive dense real matrix of size (\(m\) + 1, 1) returns a tuple (f,Df,H).fandDfare defined as above.His a square dense or sparse real matrix of size (\(n\), \(n\)), whose lower triangular part contains the lower triangular part of\[z_0 \nabla^2f_0(x) + z_1 \nabla^2f_1(x) + \cdots + z_m \nabla^2f_m(x).\]If

Fis called with two arguments, it can be assumed that \(x\) is in the domain of \(f\).

The linear inequalities are with respect to a cone \(C\) defined as a Cartesian product of a nonnegative orthant, a number of second-order cones, and a number of positive semidefinite cones:

\[C = C_0 \times C_1 \times \cdots \times C_M \times C_{M+1} \times \cdots \times C_{M+N}\]with

\[\begin{split}\newcommand{\reals}{{\mbox{\bf R}}} \newcommand{\svec}{\mathop{\mathbf{vec}}} \newcommand{\symm}{{\mbox{\bf S}}} \begin{split} C_0 & = \{ u \in \reals^l \;| \; u_k \geq 0, \; k=1, \ldots,l\},\\ C_{k+1} & = \{ (u_0, u_1) \in \reals \times \reals^{r_{k}-1} \; | \; u_0 \geq \|u_1\|_2 \}, \quad k=0,\ldots, M-1, \\ C_{k+M+1} & = \left\{ \svec(u) \; | \; u \in \symm^{t_k}_+ \right\}, \quad k=0,\ldots,N-1. \end{split}\end{split}\]Here \(\mathbf{vec}(u)\) denotes a symmetric matrix \(u\) stored as a vector in column major order.

The arguments

handbare real single-column dense matrices.GandAare real dense or sparse matrices. The default values forAandbare sparse matrices with zero rows, meaning that there are no equality constraints. The number of rows ofGandhis equal to\[K = l + \sum_{k=0}^{M-1} r_k + \sum_{k=0}^{N-1} t_k^2.\]The columns of

Gandhare vectors in\[\newcommand{\reals}{{\mbox{\bf R}}} \reals^l \times \reals^{r_0} \times \cdots \times \reals^{r_{M-1}} \times \reals^{t_0^2} \times \cdots \times \reals^{t_{N-1}^2},\]where the last \(N\) components represent symmetric matrices stored in column major order. The strictly upper triangular entries of these matrices are not accessed (i.e., the symmetric matrices are stored in the

'L'-type column major order used in theblasandlapackmodules).The argument

dimsis a dictionary with the dimensions of the cones. It has three fields.dims['l']:- \(l\), the dimension of the nonnegative orthant (a nonnegative integer).

dims['q']:- \([r_0, \ldots, r_{M-1}]\), a list with the dimensions of the second-order cones (positive integers).

dims['s']:- \([t_0, \ldots, t_{N-1}]\), a list with the dimensions of the positive semidefinite cones (nonnegative integers).

The default value of

dimsis{'l': h.size[0], 'q': [], 's': []}, i.e., the default assumption is that the linear inequalities are componentwise inequalities.The role of the optional argument

kktsolveris explained in the section Exploiting Structure.cpreturns a dictionary that contains the result and information about the accuracy of the solution. The most important fields have keys'status','x','snl','sl','y','znl','zl'. The possible values of the'status'key are:'optimal'In this case the

'x'entry of the dictionary is the primal optimal solution, the'snl'and'sl'entries are the corresponding slacks in the nonlinear and linear inequality constraints, and the'znl','zl'and'y'entries are the optimal values of the dual variables associated with the nonlinear inequalities, the linear inequalities, and the linear equality constraints. These vectors approximately satisfy the Karush-Kuhn-Tucker (KKT) conditions\[ \begin{align}\begin{aligned}\nabla f_0(x) + D\tilde f(x)^T z_\mathrm{nl} + G^T z_\mathrm{l} + A^T y = 0,\\\tilde f(x) + s_\mathrm{nl} = 0, \quad k=1,\ldots,m, \qquad Gx + s_\mathrm{l} = h, \qquad Ax = b,\\s_\mathrm{nl}\succeq 0, \qquad s_\mathrm{l}\succeq 0, \qquad z_\mathrm{nl} \succeq 0, \qquad z_\mathrm{l} \succeq 0,\\s_\mathrm{nl}^T z_\mathrm{nl} + s_\mathrm{l}^T z_\mathrm{l} = 0\end{aligned}\end{align} \]where \(\tilde f = (f_1,\ldots, f_m)\).

'unknown'- This indicates that the algorithm terminated before a solution was

found, due to numerical difficulties or because the maximum number

of iterations was reached. The

'x','snl','sl','y','znl', and'zl'entries contain the iterates when the algorithm terminated.

cpsolves the problem by applyingcplto the epigraph form problem\[\begin{split}\begin{array}{ll} \mbox{minimize} & t \\ \mbox{subject to} & f_0(x) \leq t \\ & f_k(x) \leq 0, \quad k =1, \ldots, m \\ & Gx \preceq h \\ & Ax = b. \end{array}\end{split}\]The other entries in the output dictionary of

cpdescribe the accuracy of the solution and are copied from the output ofcplapplied to this epigraph form problem.cprequires that the problem is strictly primal and dual feasible and that\[\newcommand{\Rank}{\mathop{\bf rank}} \Rank(A) = p, \qquad \Rank \left( \left[ \begin{array}{cccccc} \sum_{k=0}^m z_k \nabla^2 f_k(x) & A^T & \nabla f_1(x) & \cdots \nabla f_m(x) & G^T \end{array} \right] \right) = n,\]for all \(x\) and all positive \(z\).

- Example: equality constrained analytic centering

The equality constrained analytic centering problem is defined as

\[\begin{split}\begin{array}{ll} \mbox{minimize} & -\sum\limits_{i=1}^m \log x_i \\ \mbox{subject to} & Ax = b. \end{array}\end{split}\]The function

acentdefined below solves the problem, assuming it is solvable.from cvxopt import solvers, matrix, spdiag, log def acent(A, b): m, n = A.size def F(x=None, z=None): if x is None: return 0, matrix(1.0, (n,1)) if min(x) <= 0.0: return None f = -sum(log(x)) Df = -(x**-1).T if z is None: return f, Df H = spdiag(z[0] * x**-2) return f, Df, H return solvers.cp(F, A=A, b=b)['x']

- Example: robust least-squares

The function

roblsdefined below solves the unconstrained problem\[\begin{array}{ll} \mbox{minimize} & \sum\limits_{k=1}^m \phi((Ax-b)_k), \end{array} \qquad \phi(u) = \sqrt{\rho + u^2},\]where \(A \in\mathbf{R}^{m\times n}\).

from cvxopt import solvers, matrix, spdiag, sqrt, div def robls(A, b, rho): m, n = A.size def F(x=None, z=None): if x is None: return 0, matrix(0.0, (n,1)) y = A*x-b w = sqrt(rho + y**2) f = sum(w) Df = div(y, w).T * A if z is None: return f, Df H = A.T * spdiag(z[0]*rho*(w**-3)) * A return f, Df, H return solvers.cp(F)['x']

Example: analytic centering with cone constraints

\[\begin{split}\begin{array}{ll} \mbox{minimize} & -\log(1-x_1^2) -\log(1-x_2^2) -\log(1-x_3^2) \\ \mbox{subject to} & \|x\|_2 \leq 1 \\ & x_1 \left[\begin{array}{rrr} -21 & -11 & 0 \\ -11 & 10 & 8 \\ 0 & 8 & 5 \end{array}\right] + x_2 \left[\begin{array}{rrr} 0 & 10 & 16 \\ 10 & -10 & -10 \\ 16 & -10 & 3 \end{array}\right] + x_3 \left[\begin{array}{rrr} -5 & 2 & -17 \\ 2 & -6 & 8 \\ -17 & -7 & 6 \end{array}\right] \preceq \left[\begin{array}{rrr} 20 & 10 & 40 \\ 10 & 80 & 10 \\ 40 & 10 & 15 \end{array}\right]. \end{array}\end{split}\]from cvxopt import matrix, log, div, spdiag, solvers def F(x = None, z = None): if x is None: return 0, matrix(0.0, (3,1)) if max(abs(x)) >= 1.0: return None u = 1 - x**2 val = -sum(log(u)) Df = div(2*x, u).T if z is None: return val, Df H = spdiag(2 * z[0] * div(1 + x**2, u**2)) return val, Df, H G = matrix([ [0., -1., 0., 0., -21., -11., 0., -11., 10., 8., 0., 8., 5.], [0., 0., -1., 0., 0., 10., 16., 10., -10., -10., 16., -10., 3.], [0., 0., 0., -1., -5., 2., -17., 2., -6., 8., -17., -7., 6.] ]) h = matrix([1.0, 0.0, 0.0, 0.0, 20., 10., 40., 10., 80., 10., 40., 10., 15.]) dims = {'l': 0, 'q': [4], 's': [3]} sol = solvers.cp(F, G, h, dims) print(sol['x']) [ 4.11e-01] [ 5.59e-01] [-7.20e-01]

Problems with Linear Objectives¶

-

cvxopt.solvers.cpl(c, F[, G, h[, dims[, A, b[, kktsolver]]]])¶ Solves a convex optimization problem with a linear objective

\[\begin{split}\begin{array}{ll} \mbox{minimize} & c^T x \\ \mbox{subject to} & f_k(x) \leq 0, \quad k=0,\ldots,m-1 \\ & G x \preceq h \\ & A x = b. \end{array}\end{split}\]cis a real single-column dense matrix.Fis a function that evaluates the nonlinear constraint functions. It must handle the following calling sequences.F()returns a tuple (m,x0), wheremis the number of nonlinear constraints andx0is a point in the domain of \(f\).x0is a dense real matrix of size (\(n\), 1).F(x), withxa dense real matrix of size (\(n\), 1), returns a tuple (f,Df).fis a dense real matrix of size (\(m\), 1), withf[k]equal to \(f_k(x)\).Dfis a dense or sparse real matrix of size (\(m\), \(n\)) withDf[k,:]equal to the transpose of the gradient \(\nabla f_k(x)\). If \(x\) is not in the domain of \(f\),F(x)returnsNoneor a tuple (None,None).F(x,z), withxa dense real matrix of size (\(n\), 1) andza positive dense real matrix of size (\(m\), 1) returns a tuple (f,Df,H).fandDfare defined as above.His a square dense or sparse real matrix of size (\(n\), \(n\)), whose lower triangular part contains the lower triangular part of\[z_0 \nabla^2f_0(x) + z_1 \nabla^2f_1(x) + \cdots + z_{m-1} \nabla^2f_{m-1}(x).\]If

Fis called with two arguments, it can be assumed that \(x\) is in the domain of \(f\).

The linear inequalities are with respect to a cone \(C\) defined as a Cartesian product of a nonnegative orthant, a number of second-order cones, and a number of positive semidefinite cones:

\[C = C_0 \times C_1 \times \cdots \times C_M \times C_{M+1} \times \cdots \times C_{M+N}\]with

\[\begin{split}\newcommand{\reals}{{\mbox{\bf R}}} \newcommand{\svec}{\mathop{\mathbf{vec}}} \newcommand{\symm}{{\mbox{\bf S}}} \begin{split} C_0 &= \{ u \in \reals^l \;| \; u_k \geq 0, \; k=1, \ldots,l\}, \\ C_{k+1} &= \{ (u_0, u_1) \in \reals \times \reals^{r_{k}-1} \; | \; u_0 \geq \|u_1\|_2 \}, \quad k=0,\ldots, M-1, \\ C_{k+M+1} &= \left\{ \svec(u) \; | \; u \in \symm^{t_k}_+ \right\}, \quad k=0,\ldots,N-1. \end{split}\end{split}\]Here \(\mathbf{vec}(u)\) denotes a symmetric matrix \(u\) stored as a vector in column major order.

The arguments

handbare real single-column dense matrices.GandAare real dense or sparse matrices. The default values forAandbare sparse matrices with zero rows, meaning that there are no equality constraints. The number of rows ofGandhis equal to\[K = l + \sum_{k=0}^{M-1} r_k + \sum_{k=0}^{N-1} t_k^2.\]The columns of

Gandhare vectors in\[\newcommand{\reals}{{\mbox{\bf R}}} \reals^l \times \reals^{r_0} \times \cdots \times \reals^{r_{M-1}} \times \reals^{t_0^2} \times \cdots \times \reals^{t_{N-1}^2},\]where the last \(N\) components represent symmetric matrices stored in column major order. The strictly upper triangular entries of these matrices are not accessed (i.e., the symmetric matrices are stored in the

'L'-type column major order used in theblasandlapackmodules.The argument

dimsis a dictionary with the dimensions of the cones. It has three fields.dims['l']:- \(l\), the dimension of the nonnegative orthant (a nonnegative integer).

dims['q']:- \([r_0, \ldots, r_{M-1}]\), a list with the dimensions of the second-order cones (positive integers).

dims['s']:- \([t_0, \ldots, t_{N-1}]\), a list with the dimensions of the positive semidefinite cones (nonnegative integers).

The default value of

dimsis{'l': h.size[0], 'q': [], 's': []}, i.e., the default assumption is that the linear inequalities are componentwise inequalities.The role of the optional argument

kktsolveris explained in the section Exploiting Structure.cplreturns a dictionary that contains the result and information about the accuracy of the solution. The most important fields have keys'status','x','snl','sl','y','znl','zl'. The possible values of the'status'key are:'optimal'In this case the

'x'entry of the dictionary is the primal optimal solution, the'snl'and'sl'entries are the corresponding slacks in the nonlinear and linear inequality constraints, and the'znl','zl', and'y'entries are the optimal values of the dual variables associated with the nonlinear inequalities, the linear inequalities, and the linear equality constraints. These vectors approximately satisfy the Karush-Kuhn-Tucker (KKT) conditions\[ \begin{align}\begin{aligned}c + Df(x)^T z_\mathrm{nl} + G^T z_\mathrm{l} + A^T y = 0,\\f(x) + s_\mathrm{nl} = 0, \quad k=1,\ldots,m, \qquad Gx + s_\mathrm{l} = h, \qquad Ax = b,\\ s_\mathrm{nl}\succeq 0, \qquad s_\mathrm{l}\succeq 0, \qquad z_\mathrm{nl} \succeq 0, \qquad z_\mathrm{l} \succeq 0,\\s_\mathrm{nl}^T z_\mathrm{nl} + s_\mathrm{l}^T z_\mathrm{l} = 0.\end{aligned}\end{align} \]'unknown'- This indicates that the algorithm terminated before a solution was

found, due to numerical difficulties or because the maximum number

of iterations was reached. The

'x','snl','sl','y','znl', and'zl'entries contain the iterates when the algorithm terminated.

The other entries in the output dictionary describe the accuracy of the solution. The entries

'primal objective','dual objective','gap', and'relative gap'give the primal objective \(c^Tx\), the dual objective, calculated as\[c^Tx + z_\mathrm{nl}^T f(x) + z_\mathrm{l}^T (Gx - h) + y^T(Ax-b),\]the duality gap

\[s_\mathrm{nl}^T z_\mathrm{nl} + s_\mathrm{l}^T z_\mathrm{l},\]and the relative gap. The relative gap is defined as

\[\frac{\mbox{gap}}{-\mbox{primal objective}} \quad \mbox{if\ } \mbox{primal objective} < 0, \qquad \frac{\mbox{gap}}{\mbox{dual objective}} \quad \mbox{if\ } \mbox{dual objective} > 0,\]and

Noneotherwise. The entry with key'primal infeasibility'gives the residual in the primal constraints,\[\newcommand{\ones}{{\bf 1}} \frac{\| ( f(x) + s_{\mathrm{nl}}, Gx + s_\mathrm{l} - h, Ax-b ) \|_2} {\max\{1, \| ( f(x_0) + \ones, Gx_0 + \ones-h, Ax_0-b) \|_2 \}}\]where \(x_0\) is the point returned by

F(). The entry with key'dual infeasibility'gives the residual\[\newcommand{\ones}{{\bf 1}} \frac { \| c + Df(x)^Tz_\mathrm{nl} + G^Tz_\mathrm{l} + A^T y \|_2} { \max\{ 1, \| c + Df(x_0)^T\ones + G^T\ones \|_2 \} }.\]cplrequires that the problem is strictly primal and dual feasible and that\[\newcommand{\Rank}{\mathop{\bf rank}} \Rank(A) = p, \qquad \Rank\left(\left[\begin{array}{cccccc} \sum_{k=0}^{m-1} z_k \nabla^2 f_k(x) & A^T & \nabla f_0(x) & \cdots \nabla f_{m-1}(x) & G^T \end{array}\right]\right) = n,\]for all \(x\) and all positive \(z\).

- Example: floor planning

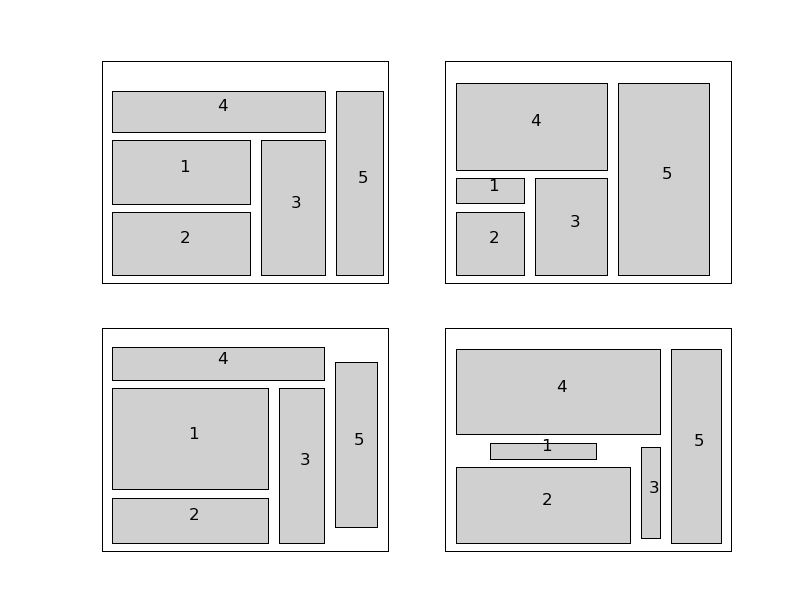

This example is the floor planning problem of section 8.8.2 in the book Convex Optimization:

\[\begin{split}\begin{array}{ll} \mbox{minimize} & W + H \\ \mbox{subject to} & A_{\mathrm{min}, k}/h_k - w_k \leq 0, \quad k=1,\ldots, 5 \\ & x_1 \geq 0, \quad x_2 \geq 0, \quad x_4 \geq 0 \\ & x_1 + w_1 + \rho \leq x_3, \quad x_2 + w_2 + \rho \leq x_3, \quad x_3 + w_3 + \rho \leq x_5, \\ & x_4 + w_4 + \rho \leq x_5, \quad x_5 + w_5 \leq W \\ & y_2 \geq 0, \quad y_3 \geq 0, \quad y_5 \geq 0 \\ & y_2 + h_2 + \rho \leq y_1, \quad y_1 + h_1 + \rho \leq y_4, y_3 + h_3 + \rho \leq y_4, \\ & y_4 + h_4 \leq H, \quad y_5 + h_5 \leq H \\ & h_k/\gamma \leq w_k \leq \gamma h_k, \quad k=1,\ldots,5. \end{array}\end{split}\]This problem has 22 variables

\[\newcommand{\reals}{{\mbox{\bf R}}} W, \qquad H, \qquad x\in\reals^5, \qquad y\in\reals^5, \qquad w\in\reals^5, \qquad h\in\reals^5,\]5 nonlinear inequality constraints, and 26 linear inequality constraints. The code belows defines a function

floorplanthat solves the problem by callingcp, then applies it to 4 instances, and creates a figure.import pylab from cvxopt import solvers, matrix, spmatrix, mul, div def floorplan(Amin): # minimize W+H # subject to Amink / hk <= wk, k = 1,..., 5 # x1 >= 0, x2 >= 0, x4 >= 0 # x1 + w1 + rho <= x3 # x2 + w2 + rho <= x3 # x3 + w3 + rho <= x5 # x4 + w4 + rho <= x5 # x5 + w5 <= W # y2 >= 0, y3 >= 0, y5 >= 0 # y2 + h2 + rho <= y1 # y1 + h1 + rho <= y4 # y3 + h3 + rho <= y4 # y4 + h4 <= H # y5 + h5 <= H # hk/gamma <= wk <= gamma*hk, k = 1, ..., 5 # # 22 Variables W, H, x (5), y (5), w (5), h (5). # # W, H: scalars; bounding box width and height # x, y: 5-vectors; coordinates of bottom left corners of blocks # w, h: 5-vectors; widths and heights of the 5 blocks rho, gamma = 1.0, 5.0 # min spacing, min aspect ratio # The objective is to minimize W + H. There are five nonlinear # constraints # # -wk + Amink / hk <= 0, k = 1, ..., 5 c = matrix(2*[1.0] + 20*[0.0]) def F(x=None, z=None): if x is None: return 5, matrix(17*[0.0] + 5*[1.0]) if min(x[17:]) <= 0.0: return None f = -x[12:17] + div(Amin, x[17:]) Df = matrix(0.0, (5,22)) Df[:,12:17] = spmatrix(-1.0, range(5), range(5)) Df[:,17:] = spmatrix(-div(Amin, x[17:]**2), range(5), range(5)) if z is None: return f, Df H = spmatrix( 2.0* mul(z, div(Amin, x[17::]**3)), range(17,22), range(17,22) ) return f, Df, H G = matrix(0.0, (26,22)) h = matrix(0.0, (26,1)) G[0,2] = -1.0 # -x1 <= 0 G[1,3] = -1.0 # -x2 <= 0 G[2,5] = -1.0 # -x4 <= 0 G[3, [2, 4, 12]], h[3] = [1.0, -1.0, 1.0], -rho # x1 - x3 + w1 <= -rho G[4, [3, 4, 13]], h[4] = [1.0, -1.0, 1.0], -rho # x2 - x3 + w2 <= -rho G[5, [4, 6, 14]], h[5] = [1.0, -1.0, 1.0], -rho # x3 - x5 + w3 <= -rho G[6, [5, 6, 15]], h[6] = [1.0, -1.0, 1.0], -rho # x4 - x5 + w4 <= -rho G[7, [0, 6, 16]] = -1.0, 1.0, 1.0 # -W + x5 + w5 <= 0 G[8,8] = -1.0 # -y2 <= 0 G[9,9] = -1.0 # -y3 <= 0 G[10,11] = -1.0 # -y5 <= 0 G[11, [7, 8, 18]], h[11] = [-1.0, 1.0, 1.0], -rho # -y1 + y2 + h2 <= -rho G[12, [7, 10, 17]], h[12] = [1.0, -1.0, 1.0], -rho # y1 - y4 + h1 <= -rho G[13, [9, 10, 19]], h[13] = [1.0, -1.0, 1.0], -rho # y3 - y4 + h3 <= -rho G[14, [1, 10, 20]] = -1.0, 1.0, 1.0 # -H + y4 + h4 <= 0 G[15, [1, 11, 21]] = -1.0, 1.0, 1.0 # -H + y5 + h5 <= 0 G[16, [12, 17]] = -1.0, 1.0/gamma # -w1 + h1/gamma <= 0 G[17, [12, 17]] = 1.0, -gamma # w1 - gamma * h1 <= 0 G[18, [13, 18]] = -1.0, 1.0/gamma # -w2 + h2/gamma <= 0 G[19, [13, 18]] = 1.0, -gamma # w2 - gamma * h2 <= 0 G[20, [14, 19]] = -1.0, 1.0/gamma # -w3 + h3/gamma <= 0 G[21, [14, 19]] = 1.0, -gamma # w3 - gamma * h3 <= 0 G[22, [15, 20]] = -1.0, 1.0/gamma # -w4 + h4/gamma <= 0 G[23, [15, 20]] = 1.0, -gamma # w4 - gamma * h4 <= 0 G[24, [16, 21]] = -1.0, 1.0/gamma # -w5 + h5/gamma <= 0 G[25, [16, 21]] = 1.0, -gamma # w5 - gamma * h5 <= 0.0 # solve and return W, H, x, y, w, h sol = solvers.cpl(c, F, G, h) return sol['x'][0], sol['x'][1], sol['x'][2:7], sol['x'][7:12], sol['x'][12:17], sol['x'][17:] pylab.figure(facecolor='w') pylab.subplot(221) Amin = matrix([100., 100., 100., 100., 100.]) W, H, x, y, w, h = floorplan(Amin) for k in range(5): pylab.fill([x[k], x[k], x[k]+w[k], x[k]+w[k]], [y[k], y[k]+h[k], y[k]+h[k], y[k]], facecolor = '#D0D0D0') pylab.text(x[k]+.5*w[k], y[k]+.5*h[k], "%d" %(k+1)) pylab.axis([-1.0, 26, -1.0, 26]) pylab.xticks([]) pylab.yticks([]) pylab.subplot(222) Amin = matrix([20., 50., 80., 150., 200.]) W, H, x, y, w, h = floorplan(Amin) for k in range(5): pylab.fill([x[k], x[k], x[k]+w[k], x[k]+w[k]], [y[k], y[k]+h[k], y[k]+h[k], y[k]], 'facecolor = #D0D0D0') pylab.text(x[k]+.5*w[k], y[k]+.5*h[k], "%d" %(k+1)) pylab.axis([-1.0, 26, -1.0, 26]) pylab.xticks([]) pylab.yticks([]) pylab.subplot(223) Amin = matrix([180., 80., 80., 80., 80.]) W, H, x, y, w, h = floorplan(Amin) for k in range(5): pylab.fill([x[k], x[k], x[k]+w[k], x[k]+w[k]], [y[k], y[k]+h[k], y[k]+h[k], y[k]], 'facecolor = #D0D0D0') pylab.text(x[k]+.5*w[k], y[k]+.5*h[k], "%d" %(k+1)) pylab.axis([-1.0, 26, -1.0, 26]) pylab.xticks([]) pylab.yticks([]) pylab.subplot(224) Amin = matrix([20., 150., 20., 200., 110.]) W, H, x, y, w, h = floorplan(Amin) for k in range(5): pylab.fill([x[k], x[k], x[k]+w[k], x[k]+w[k]], [y[k], y[k]+h[k], y[k]+h[k], y[k]], 'facecolor = #D0D0D0') pylab.text(x[k]+.5*w[k], y[k]+.5*h[k], "%d" %(k+1)) pylab.axis([-1.0, 26, -1.0, 26]) pylab.xticks([]) pylab.yticks([]) pylab.show()

Geometric Programming¶

-

cvxopt.solvers.gp(K, F, g[, G, h[, A, b]])¶ Solves a geometric program in convex form

\[\begin{split}\newcommand{\lse}{\mathop{\mathbf{lse}}} \begin{array}{ll} \mbox{minimize} & f_0(x) = \lse(F_0x+g_0) \\ \mbox{subject to} & f_i(x) = \lse(F_ix+g_i) \leq 0, \quad i=1,\ldots,m \\ & Gx \preceq h \\ & Ax=b \end{array}\end{split}\]where

\[\newcommand{\lse}{\mathop{\mathbf{lse}}} \lse(u) = \log \sum_k \exp(u_k), \qquad F = \left[ \begin{array}{cccc} F_0^T & F_1^T & \cdots & F_m^T \end{array}\right]^T, \qquad g = \left[ \begin{array}{cccc} g_0^T & g_1^T & \cdots & g_m^T \end{array}\right]^T,\]and the vector inequality denotes componentwise inequality.

Kis a list of \(m\) + 1 positive integers withK[i]equal to the number of rows in \(F_i\).Fis a dense or sparse real matrix of size(sum(K), n).gis a dense real matrix with one column and the same number of rows asF.GandAare dense or sparse real matrices. Their default values are sparse matrices with zero rows.handbare dense real matrices with one column. Their default values are matrices of size (0, 1).gpreturns a dictionary with keys'status','x','snl','sl','y','znl', and'zl'. The possible values of the'status'key are:'optimal'In this case the

'x'entry is the primal optimal solution, the'snl'and'sl'entries are the corresponding slacks in the nonlinear and linear inequality constraints. The'znl','zl', and'y'entries are the optimal values of the dual variables associated with the nonlinear and linear inequality constraints and the linear equality constraints. These values approximately satisfy\[ \begin{align}\begin{aligned}\nabla f_0(x) + \sum_{k=1}^m z_{\mathrm{nl},k} \nabla f_k(x) + G^T z_\mathrm{l} + A^T y = 0,\\f_k(x) + s_{\mathrm{nl},k} = 0, \quad k = 1,\ldots,m \qquad Gx + s_\mathrm{l} = h, \qquad Ax = b,\\s_\mathrm{nl}\succeq 0, \qquad s_\mathrm{l}\succeq 0, \qquad z_\mathrm{nl} \succeq 0, \qquad z_\mathrm{l} \succeq 0,\\s_\mathrm{nl}^T z_\mathrm{nl} + s_\mathrm{l}^T z_\mathrm{l} =0.\end{aligned}\end{align} \]'unknown'- This indicates that the algorithm terminated before a solution was

found, due to numerical difficulties or because the maximum number

of iterations was reached. The

'x','snl','sl','y','znl', and'zl'contain the iterates when the algorithm terminated.

The other entries in the output dictionary describe the accuracy of the solution, and are taken from the output of

cp.gprequires that the problem is strictly primal and dual feasible and that\[\newcommand{\Rank}{\mathop{\bf rank}} \Rank(A) = p, \qquad \Rank \left( \left[ \begin{array}{cccccc} \sum_{k=0}^m z_k \nabla^2 f_k(x) & A^T & \nabla f_1(x) & \cdots \nabla f_m(x) & G^T \end{array} \right] \right) = n,\]for all \(x\) and all positive \(z\).

As an example, we solve the small GP of section 2.4 of the paper A Tutorial on Geometric Programming. The posynomial form of the problem is

with variables \(h\), \(w\), \(d\).

from cvxopt import matrix, log, exp, solvers

Aflr = 1000.0

Awall = 100.0

alpha = 0.5

beta = 2.0

gamma = 0.5

delta = 2.0

F = matrix( [[-1., 1., 1., 0., -1., 1., 0., 0.],

[-1., 1., 0., 1., 1., -1., 1., -1.],

[-1., 0., 1., 1., 0., 0., -1., 1.]])

g = log( matrix( [1.0, 2/Awall, 2/Awall, 1/Aflr, alpha, 1/beta, gamma, 1/delta]) )

K = [1, 2, 1, 1, 1, 1, 1]

h, w, d = exp( solvers.gp(K, F, g)['x'] )

Exploiting Structure¶

By default, the functions cp and

cpl do not exploit problem

structure. Two mechanisms are provided for implementing customized solvers

that take advantage of problem structure.

- Providing a function for solving KKT equations

The most expensive step of each iteration of

cpis the solution of a set of linear equations (KKT equations) of the form(2)¶\[\begin{split}\left[\begin{array}{ccc} H & A^T & \tilde G^T \\ A & 0 & 0 \\ \tilde G & 0 & -W^T W \end{array}\right] \left[\begin{array}{c} u_x \\ u_y \\ u_z \end{array}\right] = \left[\begin{array}{c} b_x \\ b_y \\ b_z \end{array}\right],\end{split}\]where

\[H = \sum_{k=0}^m z_k \nabla^2f_k(x), \qquad \tilde G = \left[\begin{array}{cccc} \nabla f_1(x) & \cdots & \nabla f_m(x) & G^T \end{array}\right]^T.\]The matrix \(W\) depends on the current iterates and is defined as follows. Suppose

\[\newcommand{\svec}{\mathop{\mathbf{vec}}} u = \left( u_\mathrm{nl}, \; u_\mathrm{l}, \; u_{\mathrm{q},0}, \; \ldots, \; u_{\mathrm{q},M-1}, \; \svec{(u_{\mathrm{s},0})}, \; \ldots, \; \svec{(u_{\mathrm{s},N-1})} \right), \qquad\]where

\[\newcommand{\reals}{{\mbox{\bf R}}} \newcommand{\symm}{{\mbox{\bf S}}} u_\mathrm{nl} \in \reals^m, \qquad u_\mathrm{l} \in \reals^l, \qquad u_{\mathrm{q},k} \in \reals^{r_k}, \quad k = 0, \ldots, M-1, \qquad u_{\mathrm{s},k} \in \symm^{t_k}, \quad k = 0, \ldots, N-1.\]Then \(W\) is a block-diagonal matrix,

\[\newcommand{\svec}{\mathop{\mathbf{vec}}} Wu = \left( W_\mathrm{nl} u_\mathrm{nl}, \; W_\mathrm{l} u_\mathrm{l}, \; W_{\mathrm{q},0} u_{\mathrm{q},0}, \; \ldots, \; W_{\mathrm{q},M-1} u_{\mathrm{q},M-1},\; W_{\mathrm{s},0} \svec{(u_{\mathrm{s},0})}, \; \ldots, \; W_{\mathrm{s},N-1} \svec{(u_{\mathrm{s},N-1})} \right)\]with the following diagonal blocks.

The first block is a positive diagonal scaling with a vector \(d_{\mathrm{nl}}\):

\[\newcommand{\diag}{\mbox{\bf diag}\,} W_\mathrm{nl} = \diag(d_\mathrm{nl}), \qquad W_\mathrm{nl}^{-1} = \diag(d_\mathrm{nl})^{-1}.\]This transformation is symmetric:

\[W_\mathrm{nl}^T = W_\mathrm{nl}.\]The second block is a positive diagonal scaling with a vector \(d_{\mathrm{l}}\):

\[\newcommand{\diag}{\mbox{\bf diag}\,} W_\mathrm{l} = \diag(d_\mathrm{l}), \qquad W_\mathrm{l}^{-1} = \diag(d_\mathrm{l})^{-1}.\]This transformation is symmetric:

\[W_\mathrm{l}^T = W_\mathrm{l}.\]The next \(M\) blocks are positive multiples of hyperbolic Householder transformations:

\[W_{\mathrm{q},k} = \beta_k ( 2 v_k v_k^T - J), \qquad W_{\mathrm{q},k}^{-1} = \frac{1}{\beta_k} ( 2 Jv_k v_k^T J - J), \qquad k = 0,\ldots,M-1,\]where

\[\begin{split}\beta_k > 0, \qquad v_{k0} > 0, \qquad v_k^T Jv_k = 1, \qquad J = \left[\begin{array}{cc} 1 & 0 \\ 0 & -I \end{array}\right].\end{split}\]These transformations are also symmetric:

\[W_{\mathrm{q},k}^T = W_{\mathrm{q},k}.\]The last \(N\) blocks are congruence transformations with nonsingular matrices:

\[\newcommand{\svec}{\mathop{\mathbf{vec}}} W_{\mathrm{s},k} \svec{(u_{\mathrm{s},k})} = \svec{(r_k^T u_{\mathrm{s},k} r_k)}, \qquad W_{\mathrm{s},k}^{-1} \svec{(u_{\mathrm{s},k})} = \svec{(r_k^{-T} u_{\mathrm{s},k} r_k^{-1})}, \qquad k = 0,\ldots,N-1.\]In general, this operation is not symmetric, and

\[\newcommand{\svec}{\mathop{\mathbf{vec}}} W_{\mathrm{s},k}^T \svec{(u_{\mathrm{s},k})} = \svec{(r_k u_{\mathrm{s},k} r_k^T)}, \qquad \qquad W_{\mathrm{s},k}^{-T} \svec{(u_{\mathrm{s},k})} = \svec{(r_k^{-1} u_{\mathrm{s},k} r_k^{-T})}, \qquad k = 0,\ldots,N-1.\]

It is often possible to exploit problem structure to solve (2) faster than by standard methods. The last argument

kktsolverofcpallows the user to supply a Python function for solving the KKT equations. This function will be called asf = kktsolver(x, z, W). The argumentxis the point at which the derivatives in the KKT matrix are evaluated.zis a positive vector of length it \(m\) + 1, containing the coefficients in the 1,1 block \(H\).Wis a dictionary that contains the parameters of the scaling:W['dnl']is the positive vector that defines the diagonal scaling for the nonlinear inequalities.W['dnli']is its componentwise inverse.W['d']is the positive vector that defines the diagonal scaling for the componentwise linear inequalities.W['di']is its componentwise inverse.W['beta']andW['v']are lists of length \(M\) with the coefficients and vectors that define the hyperbolic Householder transformations.W['r']is a list of length \(N\) with the matrices that define the the congruence transformations.W['rti']is a list of length \(N\) with the transposes of the inverses of the matrices inW['r'].

The function call

f = kktsolver(x, z, W)should return a routine for solving the KKT system (2) defined byx,z,W. It will be called asf(bx, by, bz). On entry,bx,by,bzcontain the right-hand side. On exit, they should contain the solution of the KKT system, with the last component scaled, i.e., on exit,\[b_x := u_x, \qquad b_y := u_y, \qquad b_z := W u_z.\]The role of the argument

kktsolverin the functioncplis similar, except that in (2),\[H = \sum_{k=0}^{m-1} z_k \nabla^2f_k(x), \qquad \tilde G = \left[\begin{array}{cccc} \nabla f_0(x) & \cdots & \nabla f_{m-1}(x) & G^T \end{array}\right]^T.\]- Specifying constraints via Python functions

In the default use of

cp, the argumentsGandAare the coefficient matrices in the constraints of (2). It is also possible to specify these matrices by providing Python functions that evaluate the corresponding matrix-vector products and their adjoints.If the argument

Gofcpis a Python function, thenG(u, v[, alpha = 1.0, beta = 0.0, trans = 'N'])should evaluates the matrix-vector products\[v := \alpha Gu + \beta v \quad (\mathrm{trans} = \mathrm{'N'}), \qquad v := \alpha G^T u + \beta v \quad (\mathrm{trans} = \mathrm{'T'}).\]Similarly, if the argument

Ais a Python function, thenA(u, v[, alpha = 1.0, beta = 0.0, trans = 'N'])should evaluate the matrix-vector products\[v \alpha Au + \beta v \quad (\mathrm{trans} = \mathrm{'N'}), \qquad v := \alpha A^T u + \beta v \quad (\mathrm{trans} = \mathrm{'T'}).\]In a similar way, when the first argument

Fofcpreturns matrices of first derivatives or second derivativesDf,H, these matrices can be specified as Python functions. IfDfis a Python function, thenDf(u, v[, alpha = 1.0, beta = 0.0, trans = 'N'])should evaluate the matrix-vector products\[v := \alpha Df(x) u + \beta v \quad (\mathrm{trans} = \mathrm{'N'}), \qquad v := \alpha Df(x)^T u + \beta v \quad (\mathrm{trans} = \mathrm{'T'}).\]If

His a Python function, thenH(u, v[, alpha, beta])should evaluate the matrix-vector product\[v := \alpha H u + \beta v.\]

If

G,A,Df, orHare Python functions, then the argumentkktsolvermust also be provided.

As an example, we consider the unconstrained problem

where \(A\) is an \(m\) by \(n\) matrix with \(m\) less than \(n\). The Hessian of the objective is diagonal plus a low-rank term:

We can exploit this property when solving (2) by applying the matrix inversion lemma. We first solve

and then obtain

The following code follows this method. It also uses BLAS functions for matrix-matrix and matrix-vector products.

from cvxopt import matrix, spdiag, mul, div, log, blas, lapack, solvers, base

def l2ac(A, b):

"""

Solves

minimize (1/2) * ||A*x-b||_2^2 - sum log (1-xi^2)

assuming A is m x n with m << n.

"""

m, n = A.size

def F(x = None, z = None):

if x is None:

return 0, matrix(0.0, (n,1))

if max(abs(x)) >= 1.0:

return None

# r = A*x - b

r = -b

blas.gemv(A, x, r, beta = -1.0)

w = x**2

f = 0.5 * blas.nrm2(r)**2 - sum(log(1-w))

# gradf = A'*r + 2.0 * x ./ (1-w)

gradf = div(x, 1.0 - w)

blas.gemv(A, r, gradf, trans = 'T', beta = 2.0)

if z is None:

return f, gradf.T

else:

def Hf(u, v, alpha = 1.0, beta = 0.0):

# v := alpha * (A'*A*u + 2*((1+w)./(1-w)).*u + beta *v

v *= beta

v += 2.0 * alpha * mul(div(1.0+w, (1.0-w)**2), u)

blas.gemv(A, u, r)

blas.gemv(A, r, v, alpha = alpha, beta = 1.0, trans = 'T')

return f, gradf.T, Hf

# Custom solver for the Newton system

#

# z[0]*(A'*A + D)*x = bx

#

# where D = 2 * (1+x.^2) ./ (1-x.^2).^2. We apply the matrix inversion

# lemma and solve this as

#

# (A * D^-1 *A' + I) * v = A * D^-1 * bx / z[0]

# D * x = bx / z[0] - A'*v.

S = matrix(0.0, (m,m))

v = matrix(0.0, (m,1))

def Fkkt(x, z, W):

ds = (2.0 * div(1 + x**2, (1 - x**2)**2))**-0.5

Asc = A * spdiag(ds)

blas.syrk(Asc, S)

S[::m+1] += 1.0

lapack.potrf(S)

a = z[0]

def g(x, y, z):

x[:] = mul(x, ds) / a

blas.gemv(Asc, x, v)

lapack.potrs(S, v)

blas.gemv(Asc, v, x, alpha = -1.0, beta = 1.0, trans = 'T')

x[:] = mul(x, ds)

return g

return solvers.cp(F, kktsolver = Fkkt)['x']

Algorithm Parameters¶

The following algorithm control parameters are accessible via the

dictionary solvers.options. By default the dictionary

is empty and the default values of the parameters are used.

One can change the parameters in the default solvers by adding entries with the following key values.

'show_progress'TrueorFalse; turns the output to the screen on or off (default:True).'maxiters'- maximum number of iterations (default:

100). 'abstol'- absolute accuracy (default:

1e-7). 'reltol'- relative accuracy (default:

1e-6). 'feastol'- tolerance for feasibility conditions (default:

1e-7). 'refinement'- number of iterative refinement steps when solving KKT equations

(default:

1).

For example the command

>>> from cvxopt import solvers

>>> solvers.options['show_progress'] = False

turns off the screen output during calls to the solvers. The tolerances

abstol, reltol and feastol have the

following meaning in cpl.

cpl returns with status 'optimal' if

where \(x_0\) is the point returned by F(), and

where

The functions cp and

gp call cpl and hence use the

same stopping criteria (with \(x_0 = 0\) for gp).